Written by Ryan McGuine //

In many ways, it feels like the world is changing faster than it ever has, yet measures of economic productivity have been growing more slowly than any time in the last 200 years. Productivity growth has been the main driver of historically-improving living standards, leading to more food, better health, better housing, and more consumer goods. But despite growing at around 2% per year for the past few decades, productivity growth has been slowing in advanced economies around the world.

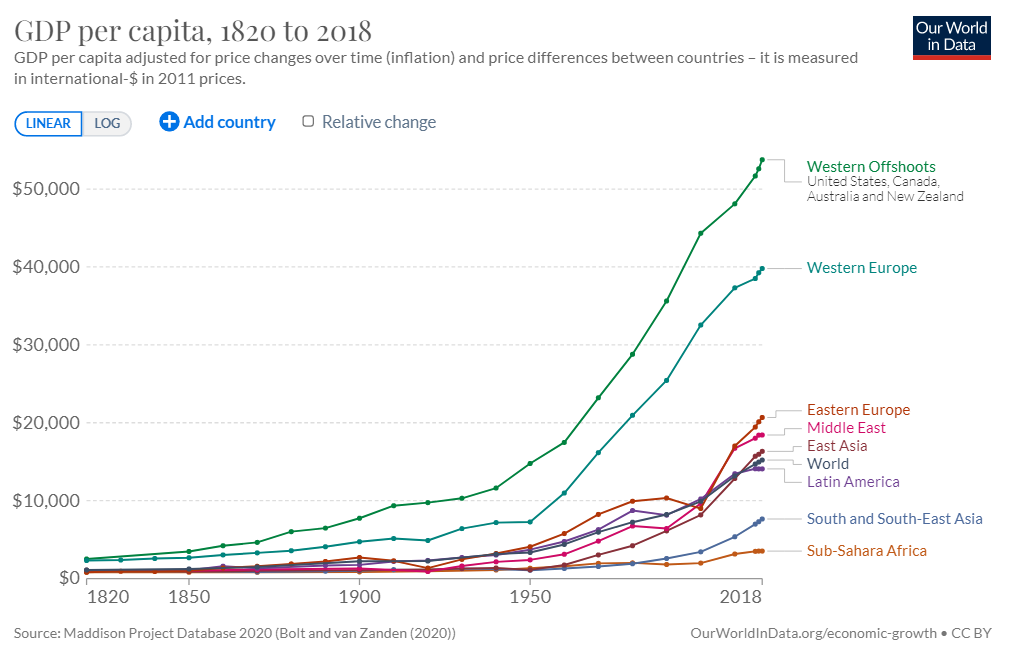

In economics, well-being is approximated by GDP per capita. While wealth is an imperfect measure of overall well-being, well-being is fundamentally about solving problems, and solving problems is easier with more resources. One conception of economic growth is as a combination of inputs (including labor, human capital, and physical capital). In this conception, getting more economic growth requires constantly increasing the amount of hours worked, education level, or products consumed. While this is a valid way to think about growth, and increasing those inputs will boost the level of economic growth, it is impossible to sustain forever. From a theoretical standpoint, changing an economy’s level of output will only temporarily change its output growth rate because returns to capital decline after a certain point. Practically, factor accumulation cannot sustain continuous growth because there are only so many resources and humans on earth.

However, this conception misses productivity, the process of using fewer inputs for a given amount of output, which also enables economic growth. Productivity includes a wide range of ideas, technologies, and innovations that make processes more efficient. In economic models, productivity is quantified by something called total factor productivity (TFP), which is the output growth that is left over after accounting for the contributions of physical and human capital. TFP is an especially blunt indicator — Robert Solow, the economist behind a commonly-used growth model, once called it a “measure of our ignorance.” It has conventionally been considered an estimate of a country’s level of codifiable technical knowledge like how to produce steel, how fertilizers affect plant growth, or how medicines combat disease, but it also probably helps to measure a society’s general economic environment, including its legal context and cultural attitudes. The notion of productivity is crucial because it establishes that modern economic growth fundamentally depends on new ideas, rather than resource consumption.

For the vast majority of human history, common measures of well-being barely changed, but economic growth really took off during the Industrial Revolution. This occurred in large part thanks to inventions like Thomas Newcomen’s steam engine, James Hargreaves’ spinning jenny, and Abraham Darby I’s coke-fired blast furnace, which used machines to do work that was once done by humans or animals. These inventions were incrementally improved on over decades of use, but even the early, inefficient versions enabled orders of magnitude more work to be done than previously. For much of the 200 years since, advances in areas like life expectancy, crop yields, and semiconductor size continued to increase rapidly in today’s rich countries, while working-age populations there grew rapidly. One way to think about this is to imagine someone travelling in time from 1880 to 1970 — they would be shocked by the differences between a world of 1bn people traveling by horses on dirt roads and living in buildings without running water, to one of 4bn people traveling by cars and planes around cities of concrete and steel. These changes place the improvements in living conditions during the last 200 years as a clear outlier by historical standards.

One leading theory for why productivity and economic growth took off during the Industrial Revolution considers the question from the supply side: the Industrial Revolution depended crucially on the widespread capabilities to invent and innovate. These include a more intentional accumulation of knowledge and better institutions to access that knowledge like libraries and universities, as well as technical skills disseminated by mechanical institutes and other professional associations. Another theory has more to do with the demand side, and says that market size and potential adoption are the key aspects behind new inventions because getting technology to the point that it can be commercialized is expensive. As such, it makes sense that the Industrial Revolution began in Britain because by world standards, its labor was expensive and energy was cheap. Both supply and demand factors probably played some role in the inception of modern, productivity-driven economic growth.

More recently, trends of increasing well-being that have prevailed in the West since the Industrial Revolution have also taken root in poor countries, causing poverty rates to fall, and access to medicine and education to increase. At the same time, however, productivity has stagnated across the developed West, and well-being with it. Productivity in key areas has fallen behind the costs of achieving additional technological gains, making it increasingly expensive to generate equivalent improvements. In this case, imagine someone travelling in time from 1970 to 2020. The same appliances would be much more energy efficient, and there would be computers. Both of those things are major improvements, but these would be less shocking to someone from a different time, and have contributed less to measured productivity. Solow once quipped, “You can see the computer age everywhere but in the productivity statistics.” By the standards of the last 200 years, the last 50 have been an outlier with respect to measured productivity growth in wealthy countries.

There are a few possible explanations for why productivity is slowing. For example, beginning in the late 1800s a huge number of “general purpose technologies” like mass production, steam engines, electricity generation and transmission, internal combustion engines, pharmaceuticals, indoor plumbing, and air travel were invented. It took a while for these inventions to begin noticeably affecting the economy, but they eventually led to a growth boom during the 1920-70s. However, that boom has petered out as societies have mostly gotten what benefits they could out of these technologies. It may be the case that new ideas are literally getting harder to find because so much has already been discovered. Alternatively, it may be that there is currently another boom period of major innovations (particularly in areas like CRISPR, RNA therapies, quantum computing, nuclear fusion, and artificial intelligence), but these inventions have yet to make a meaningful impact on the economy.

Another hypothesis is that people tend to become more interested in things like comfort, leisure, and status as they become wealthier. The productivity in certain sectors has increased at an incredible clip (consumer products like light bulbs and televisions have fallen in cost and increased in quality so quickly that using them to measure well-being across time is basically meaningless). As people become richer, they have mostly opted to take more time off work, use their extra money to buy houses in nicer neighborhoods, get additional healthcare, and send their kids to more impressive schools. These are all sectors with productivity very close to zero. So at the same time that consumers have access to a wider variety of goods and services than ever before because of their high productivity, luxury and status goods have become less available and more expensive because of their low productivity. As spending on real estate, education, and healthcare goes up, they become an ever-larger portion of the economy, and measures of average productivity become ever-smaller.

Slower productivity growth means slower economic growth, which is a problem on two counts. The first comes from taking a “levels view” — that is, economic output matters because many facets of well-being closely correlate with economic output. While not always exactly true, larger economies tend to have wealthier citizens on average, and wealthier citizens tend to be better levels of well-being on average. The other is a “rates view,” which says that economic output growth matters because a society which has access to a growing pie will be more stable than one that is constantly fighting over pieces of a fixed pie. Slowing down economic growth would not only make more people poorer for longer, but also do very little to minimize environmental degradation.

The Industrial Revolution offers some hints as to how to increase productivity going forward. On the supply side, fostering a public attitude of “improvement thinking” would be valuable, which can be done by coordinating people to solve technical and political problems, and exposing people to others like themselves who are innovating. On the demand side, policy can be used to boost productivity by removing barriers to innovation. For example, it now takes longer than ever to train scientific researchers, and overzealous IP laws slow the spread of new ideas. In the physical world, an assortment of structural problems, as well as red tape like environmental reviews and zoning rules, drive up the costs and timelines of building infrastructure. Policy can also be used to improve policies that boost innovation like funding for scientific research, and immigration and global trade reform.

Of course, there is more to life than making new things and buying consumer goods. True well-being also involves visiting with friends and family, engaging in hobbies, and a preserving a healthy environment. Since these have little monetary value, they do not contribute to measured technological or economic growth, and it is not worth grieving growth which is slower due to these factors. However, complacency is also misplaced. Humanity faces a vast array of challenges in the decades ahead, and having more resources and knowledge to combat them would be better than less resources and knowledge. The key to generating more of these lies largely in boosting productivity growth.